Outlook for the Month of September 2024

Economy Review

The key events in the month were –

-

Domestic Factors –

a) GDP – India’s GDP rose by 6.7% in Q1FY25, following 7.8% growth in Q4FY24. India continues to be the fastest growing major economy.

b) GST Collection – India’s GST collection in August’24 rose 10% yoy to Rs 1.75 tn, on the back of stable economic growth and improved compliance.

c) Manufacturing PMI – India’s Manufacturing PMI for Aug’24 came in at 57.9, above the 50-mark indicating expansion.

d) Fiscal Deficit – India’s fiscal deficit stood at 17.2% of BE in Apr- July’24 against 33.9% of BE a year ago, mainly on account of a higher RBI dividend, higher direct tax collections and sluggish expenditure on account of elections.

d) Monsoon – India experienced 16% higher than normal rainfall in Aug-24, the fifth highest in the month since 2001. Overall, the four-month (June-Sept) monsoon season is likely to report ‘above-normal’ rainfall activity.

-

Global Factors –

a) FED – US Fed Chair Jerome Powell in his statement at Jackson Hole expressed further confidence on imminent policy easing, stating that further cooling in the job market would be unwelcome and that inflation was within reach of the US central bank's 2% target.

b) Eurozone PMI – Eurozone Manufacturing PMI at 45.8 remained below the 50 mark in Aug’24, driven by the weak demand scenario. However, Services PMI reported expansion at 53.3 in Aug’24 vs. 51.9 in July’24.

c) Crude Oil – Brent crude oil prices fell to $80/bbl during the month since the OPEC+ plans to increase production in the coming months. Further, weak demand in China and the United States could exert downward pressure on crude prices going forward.

Domestic Macro Economic Data

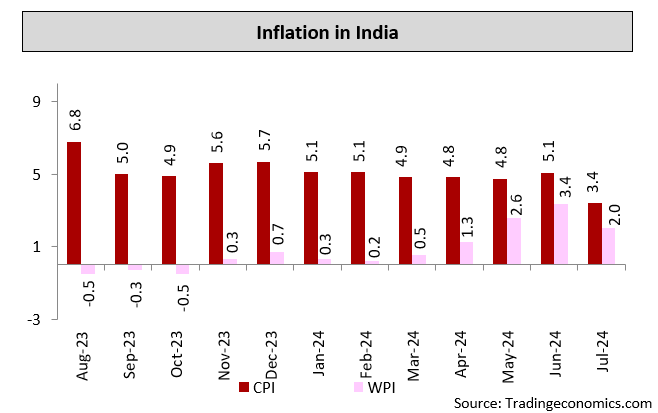

Inflation – India’s CPI moderated sharply to 3.4% in Jul’24 vs. 5.08% in June’24 due to base effect despite a continued increase in vegetable prices. India’s WPI at 2.0% in Jul’24 continues to remain benign led by softness in food prices.

Outlook for Equities

Indian markets fell sharply at the beginning of the month after a weaker-than-expected US employment data, a sell-off in Japan led by unwinding of the carry trade and geopolitical tensions in the Middle East. US Fed Chair Jerome Powell’s statement in Jackson Hole signalling imminent rate cuts, as well as greater confidence in soft landing, helped prop up emerging markets, including India.

On the domestic front, India’s fiscal deficit stood at 17.2% of BE in Apr- July’24 against 33.9% of BE a year ago, mainly on account of a higher RBI dividend, higher direct tax collections and sluggish expenditure on account of elections. India’s Manufacturing PMI for Aug’24 came in at 57.9, above the 50-mark indicating expansion. India experienced 16% higher than normal rainfall in Aug-24, the fifth highest in the month since 2001. Overall, the four-month (June-Sept) monsoon season is likely to report ‘above-normal’ rainfall activity. FIIs bought equities worth $1.2bn in the month of August’24 while DIIs remained buyers to the tune of $5.8bn.

We expect Nifty earnings to grow at ~12-13% in FY25. Indian Equity Market is currently in euphoric mode with strong momentum and has rallied 13% during the last five months driven by strong domestic flows. Post the recent rally, Nifty is currently trading at ~23x FY25e P/E. Hence, we believe that markets will consolidate for some time before the next up move. Investors can continue to invest in equities from a long-term perspective.

Outlook for Debt

RBI MPC in the month of August kept key repo rate unchanged at 6.50% and maintained stance at withdrawal of accommodation. 4 out of 6 members voted to keep the key rates unchanged and keep stance unchanged. MPC remained focussed on inflationary concerns, emanating especially from persistent food inflation side pressures. Governor highlighted households’ perception of inflation increasing, lower consumer confidence and expectations of core inflation bottoming out. Growth continues to be strong, but few indications of moderation are visible from lower than anticipated corporate profitability, general government expenditure and core industries output. In the press conference Deputy Governor Patra said neutral rate which is driven by potential growth has started to rise and current level of policy rate is just about right in that context. Concerns on liquidity management issues of banks were also highlighted as divergence between credit and deposit growth has become stark. Governor also pointed out end use of credit lending norms not being adhered to by certain entities. This has led to concerns of loan funds being deployed in unproductive or speculative purposes. RBI MPC meeting minutes continued to signal caution on inflationary risks. While the comfort on growth continued, elevated food inflation was the primary worry for most members. The internal members remain hawkish given uncertainty on both domestic and global factors while looking for more durable signs of disinflation before a shift in policy.

Banking system liquidity continues to be in a surplus mode remaining higher than Rs. 1tn for most of the month. FPI inflows in August have been above $2bn in the debt segment. Monsoon has progressed well as cumulative rainfall was 6.9% above long-term average as on August 30, 2024. Basins and reservoirs levels were around 12% above long-term average for week-ending August 29. Real GDP growth in 1QFY25 eased to a five-quarter low of 6.7%, largely led by unfavorable base effect. Growth was broad-based, with private consumption growth catching up with investment growth. CPI inflation in July fell to 3.5% from 5.1% in June supported by a favorable base despite a continued increase in vegetable prices. Core inflation at 3.3% was slightly higher than in June. WPI inflation in July fell to 2% from previous month reading of 3.4%. IIP growth in June was at 4.2% as mining and electricity production were robust. Goods trade deficit in July remained elevated at US$23.5 bn, as imports in July increased 7.5% Y-o-Y.

Global scenario remains benign as consensus has built in for rate cut by FOMC in September. The Fed Chair at the Jackson Hole conference provided little new guidance on future rate actions by the Fed. The Fed Chair said “… the time has come for policy to adjust.” Markets viewed these statements as a signal that the rate cut cycle will start from the September policy. Gold prices reached a new high of $2531.60 in August and have been in a consolidation phase since then. Brent prices declined by 2.3% during the month on demand concerns while dollar index fell 2.2% in August as markets price in easing.

In the near term, market will watch for FPI flows in gsec, August CPI data and MPC in October. Globally US non farm payroll data, CPI and Fed meeting in September are key data points. 10 year gsec closed at 6.87% on 30 August, 2024, falling by 5bps during the month. 10 year yield is likely to be in a range of 6.75%-7.00%. Spread of 10 year Gsec with corporate bonds is around 50 bps and likely to remain between 50-70 bps.